If I had to choose one metal to own it would be copper. It’s essential to nearly everything, but more importantly we’re running out…

There are two trends driving copper demand:

The energy revolution (AKA the electrification of energy)

The urbanization of underdeveloped countries (primarily Asia and Africa)

To meet demand we’re going to need to mine more copper over the next 27 years then we’ve mined in ALL of human history to date.

That would be a challenging task even IF we had the copper reserves… the problem is, we don’t.

Copper production is falling at the world’s biggest mines.

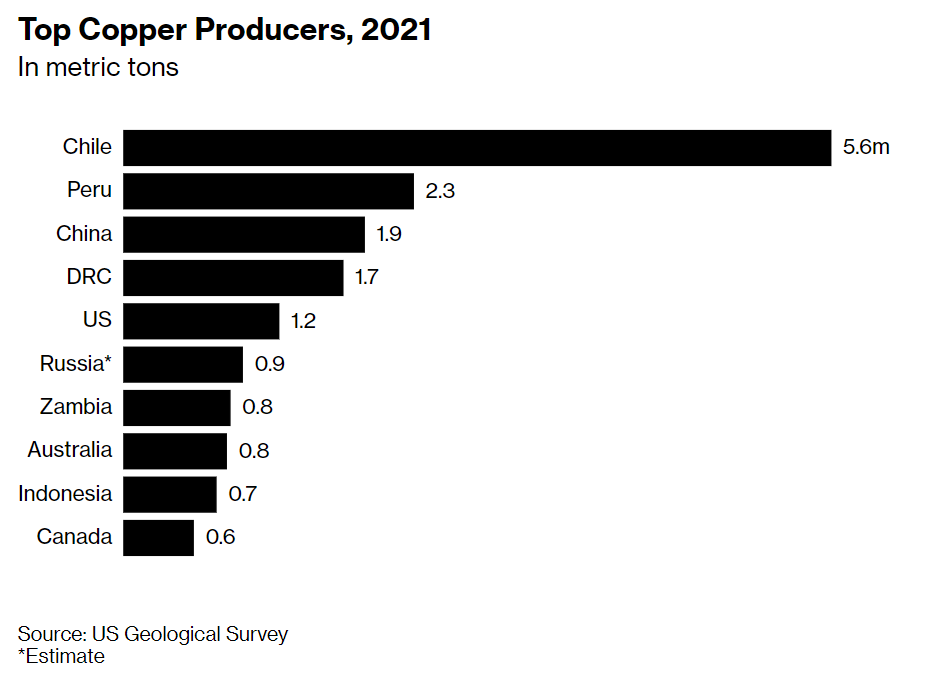

Codelco, the Chilean government-owned copper miner, is the world’s largest copper producer. And, Chile is where most of the copper comes from.

Things are not going well.

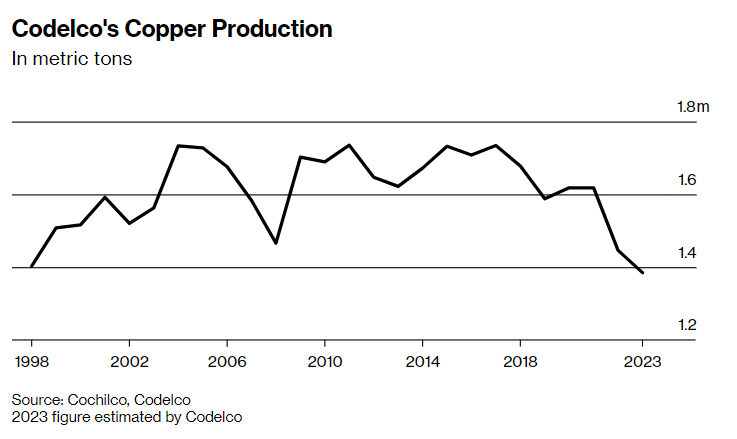

Production is at its lowest in a quarter century, costs have surged, and profits have slumped – all at a time when the world’s need for copper is greater than ever.

Codelco’s production fell more than 10% in 2022 and is set to fall another 7% this year, to 1.35 million metric tons.

This is more than a 20% drop from six years ago.

But, it is not only Codelco, ore grade is deteriorating around the world as existing deposits are mined and new ones are more difficult and costly to develop.

Codelco’s CEO said “There’s no easy mining left—not in Chile nor the rest of the world.”

Global production issues confirmed.

I came across an interesting Twitter thread looking at Q1 2023 financial statements from the biggest copper producers.

Copper production from Q1 2023 to Q1 2022, production was down ~200kt.

The biggest contributor to falling numbers is the fact that there is consistently less copper in every tonne of rock that comes out of the ground (Note: Percentage of copper per tonne of rock is known as grade.)

It is becoming more expensive to mine a pound of copper. Add to that the fact that energy and labor prices are skyrocketing.

4 of the 8 copper companies that reported cash costs saw increases of more than 20% from last quarter…

Let that sink in. 20% increase in costs in 3-months. That is insane!

All of this is to say one thing: the world’s future copper supply is seriously in trouble.

We need much higher copper prices to incentivize exploration and development. And remember, we can’t just turn on the taps and produce more Cu – It takes +10-years to bring a new copper mine online.

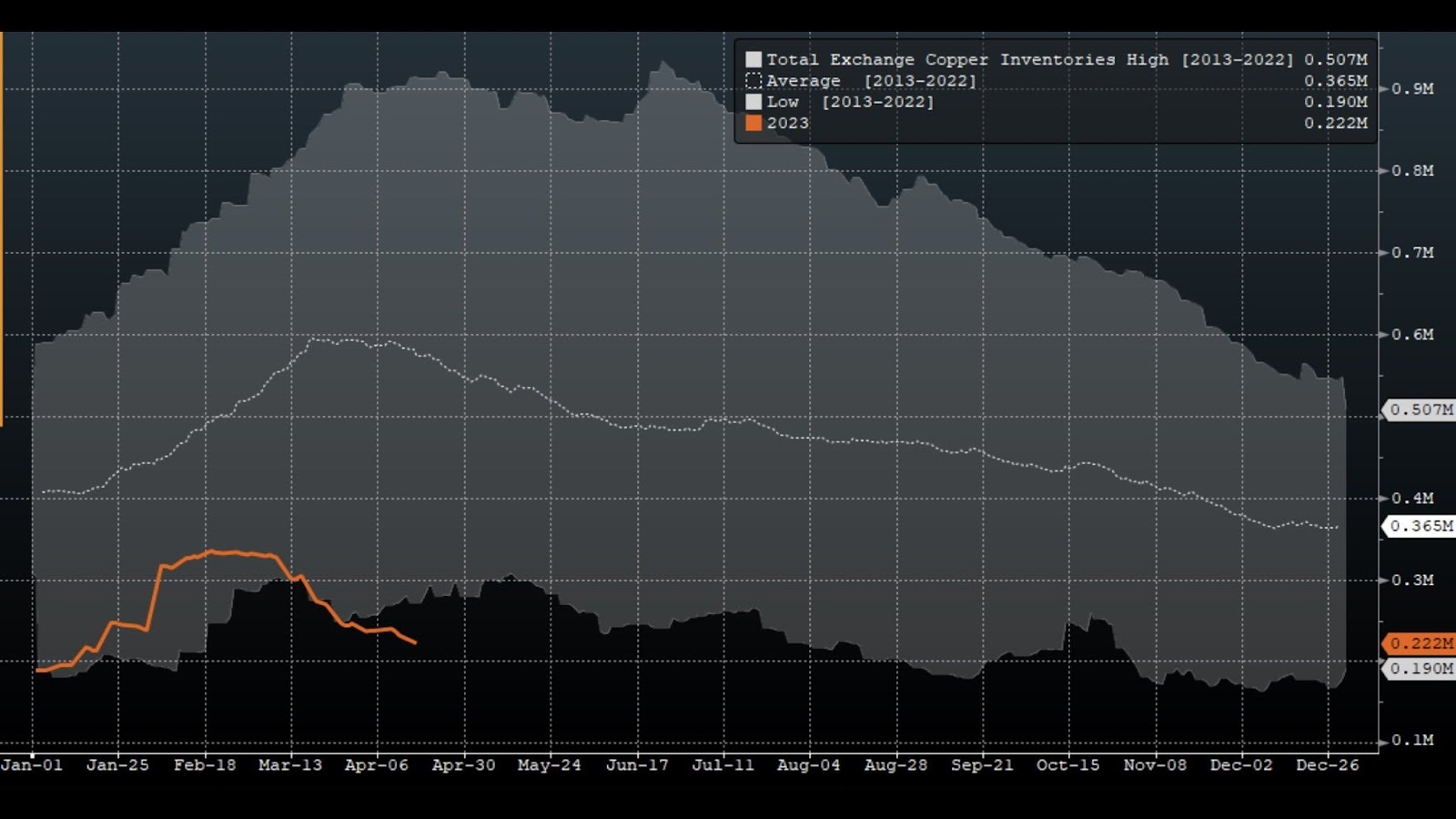

Oh, BTW Inventories are running dry…

Below is a chart of global copper inventories over the past 10 years. The gray area is the high, and low range, the white line is the average, and the orange is the 2023 inventory level.

This chart should scare you because it says one thing: the world has no copper inventories.

In summary:

Copper demand is stronger than ever.

The world’s biggest copper miner is having major production issues.

Costs are up and production is down for the world’s top 10 biggest copper producers.

Current copper inventories are lower than they have been in the past 10 years.

My takeaway is simple: Own copper or be poor.

I don’t want to be poor, and neither do Ri Members. That’s why we’re about to launch our next Ri Deal:

Project Patriot

We have one objective with this deal: BIG GAIN HUNTING.

Kazakhstan’s Chu-Sarysu is the world’s 3rd largest sediment-hosted copper basin. Yet, the region has been largely unexplored since the 1970s, but that is changing as we speak.

In 2018, the government overhauled the mining code, unlocking exploration in Kazakhstan for the first time since the collapse of the Soviet Union.

The team locked down some of the most interesting assets in the region and are applying a fresh, modern approach to discovery.

Big Data – compiled and digitized the largest privately-held exploration dataset for Central Asia.

Machine Learning – applying predictive machine learning to datasets, optimizing for the most prospective geology.

Major Partners – They have signed a joint venture agreement with one of the largest copper companies on the planet.

They are ready to drill multiple porphyry copper targets. These are the type of geological formations that have the potential to become monster deposits.

These are the types of deposits that took Filo Mining (FIL.TO) from a $200 million market cap to a $2 billion market cap.