I recently invested into American Oil and Gas royalties.

Here’s why:

Exposure to energy;

Exposure to the USA;

Exposure to cash flow;

Exposure to assets NOT listed on capital markets;

Let’s dig in…

The Case for Higher Oil

The investment case for oil and gas is pretty straight forward. It boils down to the this:

Oil is cheap, but is about to get expensive.

We believe oil prices, compared to equity markets, will revert to the mean due to significant under investment in the sector.

We are now going to walk through the market conditions that got us to this conclusion.

FACT: Oil is Cheaper than ever.

We compare oil and natural gas prices to the S&P 500 because the ratio helps give us an understanding of the true cost of energy.

When energy is “cheap” compared to the value of the S&P we can anticipate that over time this will correct. It will do so but either energy prices going up, or company valuations going down – either way you want to own energy in this environment as a means of protecting and/or growing your capital. The inverse is true when energy prices are “expensive” as we saw in the 80’s during the oil embargo.

Theoretically energy should be priced so that investors and producers make enough money to justify operating and investing in new production. But, cheap enough that consumers are not gouged at the pump and can maintain a comfortable life.

But markets do not exist in a state of equilibrium. The pendulum swings back and forth.

Right now energy is objectively cheap.

Nothing in life is certain but based on historic data we expect the pendulum is about to swing the other way.

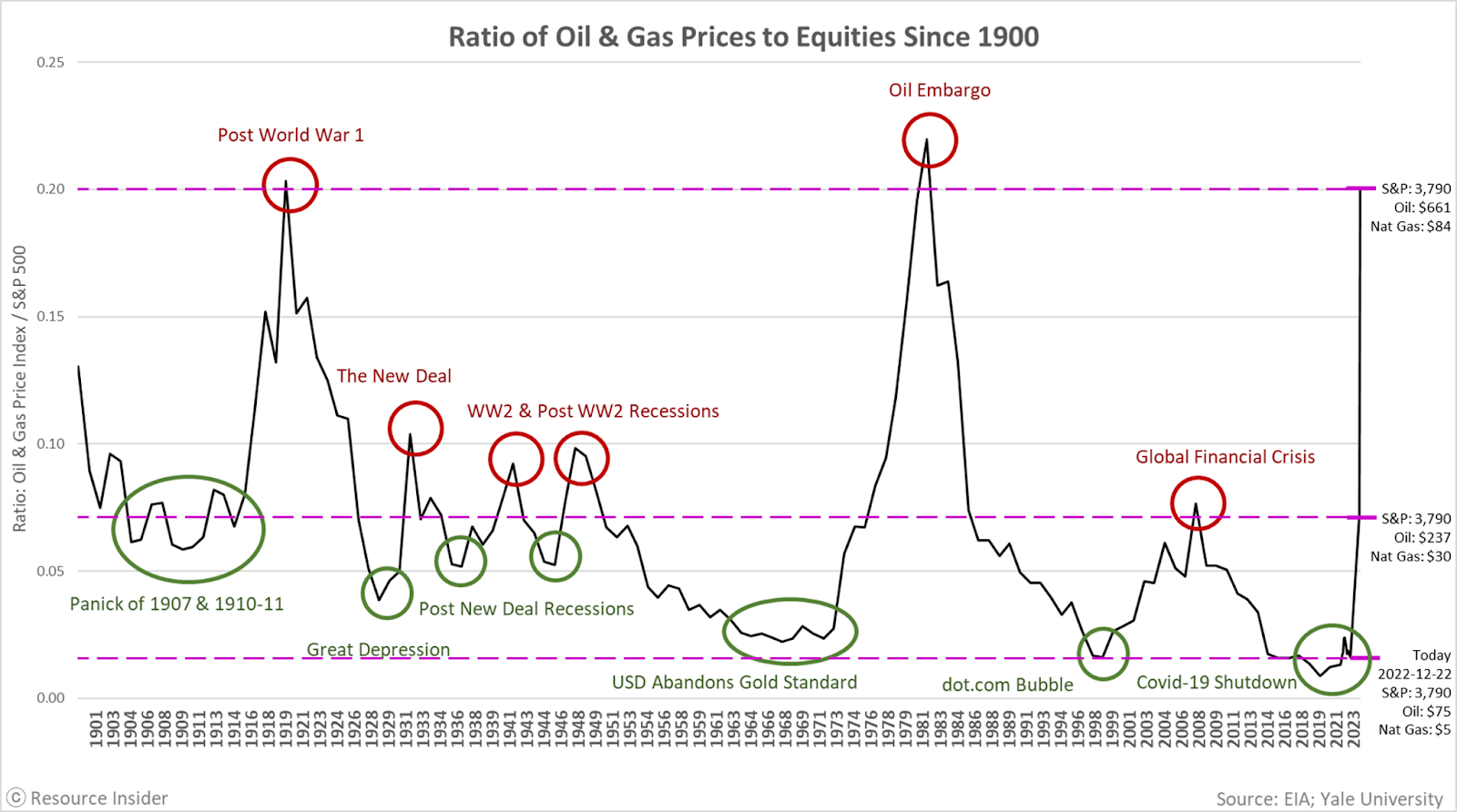

The chart below shows the price of oil compared to the S&P 500 since 1900.

Today the price of oil is ~$75/bbl and natural gas is ~$3/mcf while the S&P 500 is trading at 4,000.

Before 2020/the pandemic, oil and gas prices were the cheapest in recorded history when compared to the S&P 500.

If the ratio swings back to 2008 levels at today’s S&P 500 levels then oil will be ~$240/bbl and gas ~$30/mcf.

If the ratio reaches 1918 or 1980 levels… then the world is in for a world of hurt. Oil prices will be ~$660/bbl and natural gas will be $84/mcf.

Now, I think it is unlikely that oil prices will spike without a simultaneous pull back in the S&P – but even still I wouldn’t be surprised if we see oil prices above $150/barrel.

Even if oil prices don’t move at all (unlikely in my opinion), in the event of a major pull back in listed equities energy should act as a safe haven for capital.

Why is Oil so Cheap?

Horizontal fracturing (AKA fracking) came on the scene in a big way in the mid 2000s.

Between 2005 and 2010 the shale-gas industry in the United States grew by 45% a year. In 2005 shale gas production made up just 4% of the USAs overall gas production, by 2012 it accounted for 24%.

Meanwhile, oil prices were high. In 2008 oil price shot up to more than $140/bbl. Prices briefly crashed later that year, but quickly recovered and consistently traded around $100/bbl until 2014.

From 2005-2014 the frackers were printing money – the likes of Harrold Hamm of Continental Resources (CLR) developed the Bakken, Tom Ward and Aubrey McClendon of Chesapeake Energy (CHK) built the 2nd largest natural gas producer through a levered land grab, Charif Souki of Cheniere Energy (NYSE: LNG) built the first U.S. LNG export terminal, and Scott Sheffield at Pioneer Natural Resources led the development of the world renowned Permian Basin.

Horizontal wells came online with huge volumes of oil, but were expensive to drill.

Then the problems started.

Banks allowed the frackers to borrow against their estimated oil reserves, and so they did.

Frackers would drill, hitting oil nearly every time, but unknowingly (to most) they were significantly overestimating their reserves.

The result?

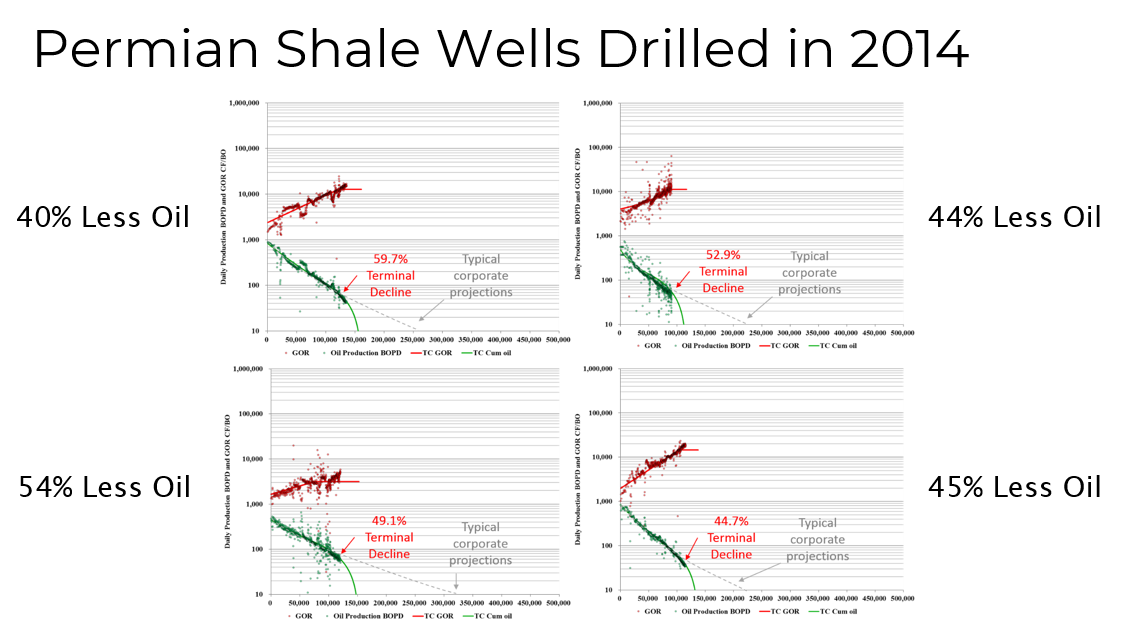

Wells would “run dry” sooner than expected… There was a lot less accessible oil than anticipated.

The above charts demonstrate well decline rates occurring far faster than anticipated.

Which is not good when borrowing based on expected production.

So what did they do?

Naturally, they drilled more wells to keep production high and meet debt payments. Inadvertently creating a pyramid scheme, with the revenue generated by new wells was required to pay off the debts on the old wells.

They drilled to borrow, and borrowed to drill.

Companies relied on rising oil prices to bail them out. But inevitably the sheer volume of oil that was being produced ensured that maintaining high prices was impossible.

More Supply = Lower Prices.

By 2018 the U.S. had grown to be the biggest oil and gas producer in the world.

A Change of Heart

Executive bonuses were tied to production, not profitability. Which brings to mind one of Charlie Munger’s favorite sayings “show me the incentive and I will show you the outcome.”

During the Covid Crash, when oil prices went negative,this all changed and executive compensation was restructured. Today, compensation is driven by profitability.

This means more disciplined balance sheets with less debt (aka less drilling). In turn, capital discipline will lead to less production, higher oil prices, and more profitable companies.

The Rusky Bailout

Then Russia invaded Ukraine and oil prices skyrocketed, saving many companies.

They took this opportunity to pay down debt, hedge production at higher prices, and start telling a different narrative (closer to the truth) to the market.

The truth is that they had “high-graded” all of the U.S. shale plays. This means that they have drilled the best and most profitable shale locations trying to make ends meet. What’s left is lower quality acreage.

This means that the U.S. shale production outlook is in bad shape.

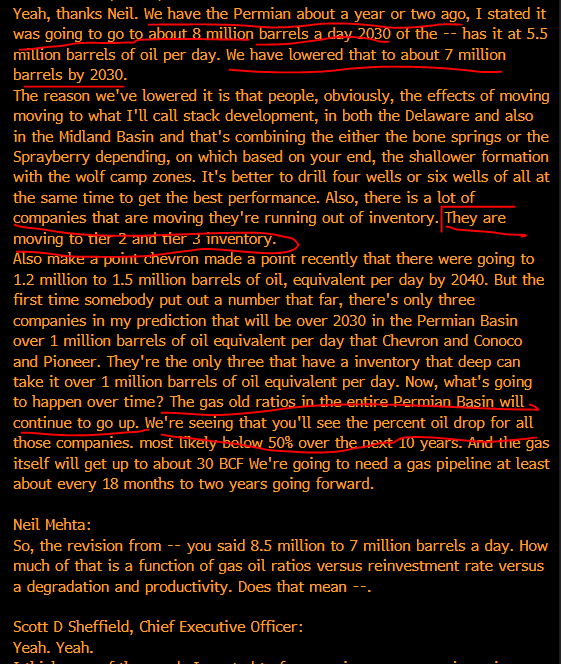

Speaking at a Goldman Sachs energy conference in Miami, Scott Sheffield, CEO U.S. shale giant Pioneer Natural Resources, said that the company has lowered its 2030 total Permian Basin oil production forecast from +8 million b/d to ~7 million b/d.

This indicates a significant slowdown in annual U.S. oil production.

Lower production means higher prices.

Will drilling come back?

It is going to take time for drilling to come back in a big way. The world at large has mismanaged invested in the energy space for two main reasons:

The Green Energy Transition

A willful blindness has infected the western world, with the claim that oil demand is somehow going to disappear in 5 or 10 years.

This is highly unlikely.

Two decades of aspirational policies and trillions of dollars in subsidies, most of it on solar, wind, and battery technologies, have yet to produce anything close to an energy transition that eliminates hydrocarbons.

Over the last 10 years $3.8 trillion has been poured into renewables, yet fossil fuel dependence has only been reduced by 1% (82% to 81% of the overall energy consumption).

The IEA (International Energy Agency) noted that an energy transition is “a shift from a fuel-intensive to a material-intensive energy system.”

They estimate the world will need to increase the supply of minerals such as lithium, graphite, nickel, and rare earths by 4,200%, 2,500%, 1,900%, and 700%, respectively, by 2040.

The world will need dozens of new world-class mines for all of these minerals, requiring tens of billions of dollars of investment to develop.

On average, it takes 16 years to bring a mine from exploration to production. So, even if we had the technology (which we don’t) and the mineral reserves (which we don’t), it is nearly impossible to provide the materials required to replace hydrocarbons for energy demand in the next 10 years.

In the interest of time I’m not going to touch on the inefficiency and the intermittency issues of renewable energies here… Instead just ask your German friends how it’s going.

Poor Returns

The frackers were so far off on production estimates that many investors watched their money get torched by aggressive drill programs.

Once upon a time any semi competent wildcatter with a half-baked idea could call up an energy PE fund and walk out with a $100m cheque. Today it is nearly impossible to find private equity money willing to drill new wells. Their mandates have been changed to buy production (where they can accurately calculate reserve estimates).

To give you an idea of how far off historic reserve estimates were, today banks discount all future annual production by 10% then discount reserve estimates by 50% before calculating how much they are willing to lend.

To incentivize this sort of investing again, oil prices are going to have to move MUCH higher.

What about today?

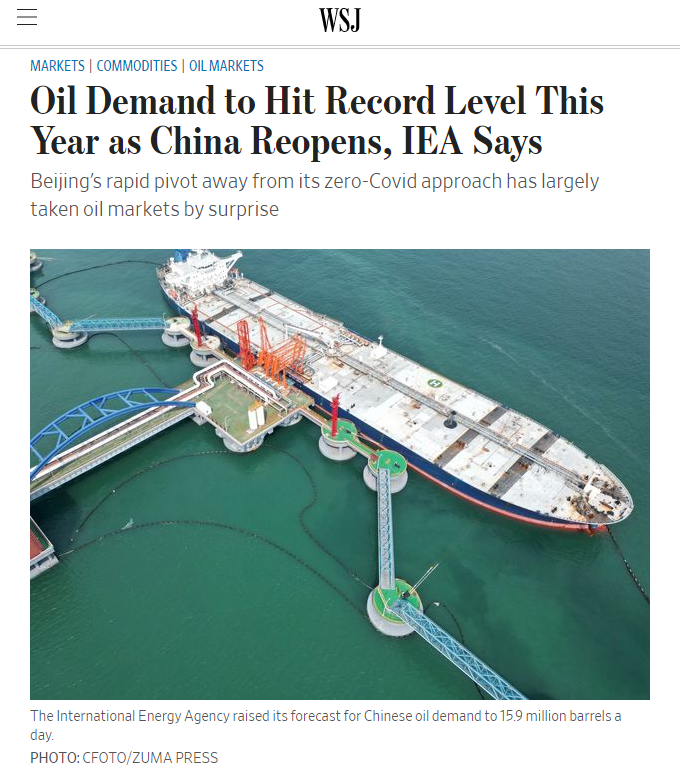

The lost energy production resulting from the Russia/Ukraine war is just the start. China’s reopening is about to shock the oil markets once again.

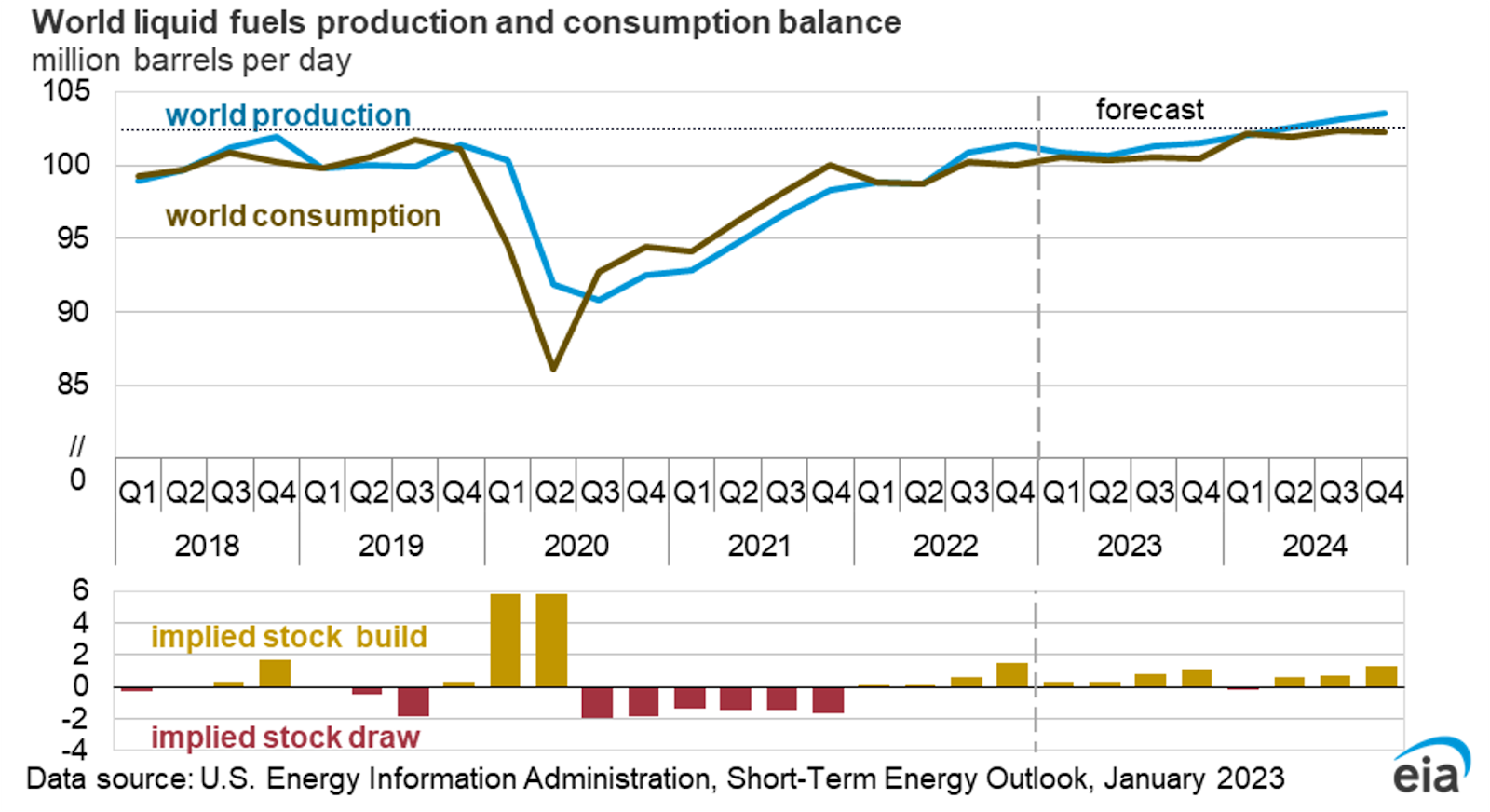

Since China reopened, the International Energy Agency (IEA) increased its 2023 forecast for oil demand growth by nearly 200,000 bbls/day to 1.9m bbls/day.

The IEA now expects 2023 total oil demand to average 101.7m barrels/day – setting new record highs.

We have already talked about that OPEC+ has been cutting production. But that’s just the tip of the iceberg….

Saudi Arabia is saying that they are maxed out on production – meaning, they don’t have the capacity to produce any more oil than they are currently producing.

Why Now?

The Russians are off the board, the Arab world is tightening production, the Chinese are ramping up the economy all whilst oil demand is peaking and USA energy reserves are dwindling.

This confluence of events has made me want to get long U.S. energy production.

BUT I want to minimize risk so I’ll be using an investment instrument you’re all familiar with: royalties.