At Resource Insider we have been talking about how gold is an antifragile investment (as volatility and uncertainty increase gold strengthens), and why the current situation in the global economy has been setting up for gold to outperform broader equity markets.

Today, the economy appears increasingly more fragile as the hours pass. Let’s discuss some of the pain points that are starting to show.

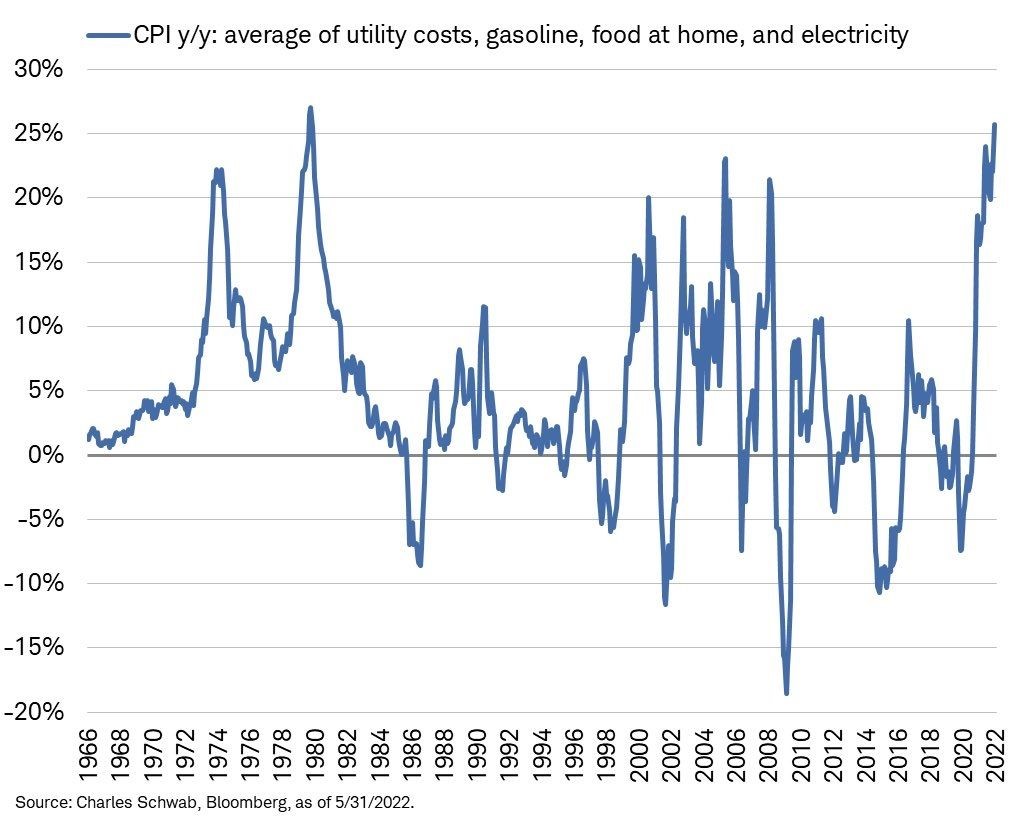

Inflation has been eating into consumer buying power as the average person’s fixed costs are skyrocketing. In May, the average cost of utilities, gasoline, food at home, and electricity printed the highest inflation number since the 1980 peak of 25.7%.

You’ll recall last year economists and politicos called inflation “transitory” declaring that consumers are “flush with cash”.

Both statements are proving to be false.

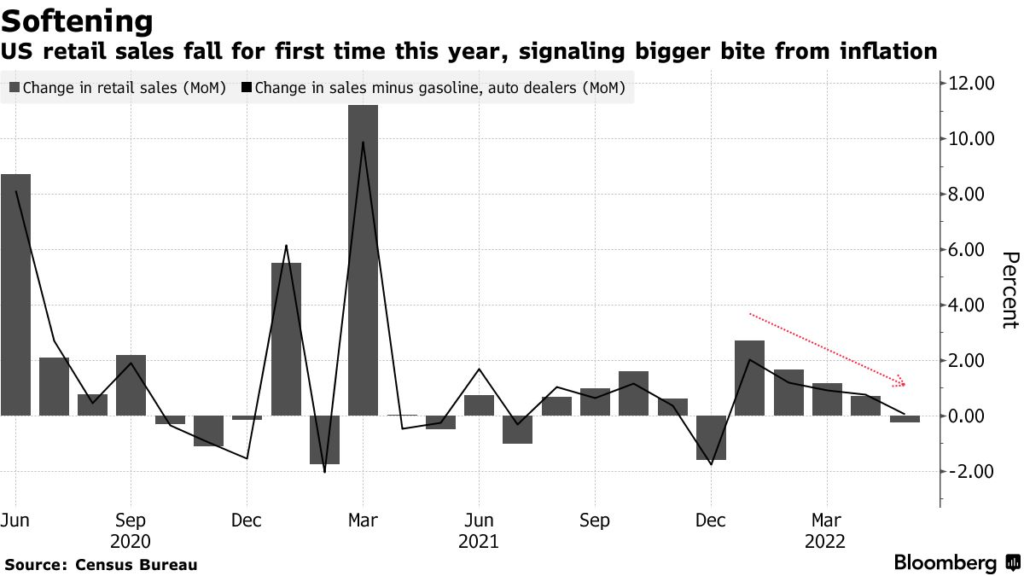

In May, US retail sales posted the first drop in five months, led by a plunge in auto sales and other big-ticket items.

Retailers such as Walmart, Gap, and others are starting to feel the pain as well. According to Bloomberg, companies that released earnings over the past 2 weeks within the S&P consumer indexes with a market cap of at least $1 billion reported that inventories rose $44.8 billion (AKA they have a bunch of stuff they can’t sell). That’s a 26% increase from this time last year.

In the past, the primary culprit behind inflation was wages. Labor is a huge component of input costs, so the Fed’s playbook to fight inflation has been to raise interest rates and increase unemployment. In the wake of globalization, the US has sustained much lower levels of unemployment without experiencing inflation.

Today’s inflationary environment is different. This wave of inflation has been driven by supply constraints, resulting in real wages going down (consumers have less purchasing power).

The Fed is fighting it by raising interest rates. In return, this is further putting a squeeze on corporate profits as the economy weakens. We are starting to see the first wave of layoffs as companies such as Netflix, Peloton, MasterClass, Coinbase, Robinhood, and Carvana have all laid off as much as 20% of their workforce. Even Tesla has announced layoffs to “keep from going bankrupt.”

Now, the cracks are starting to show in real estate.

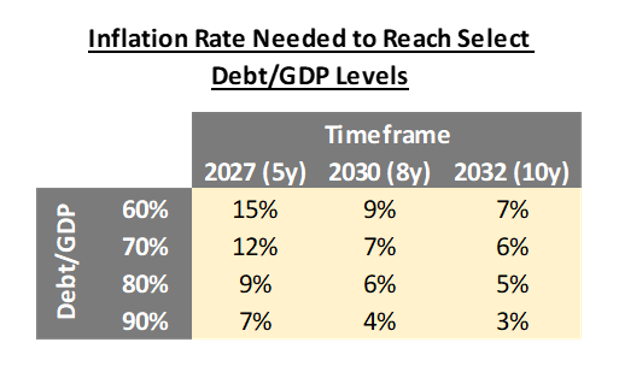

The US is in a twin deficit, meaning there is both a current account deficit and a fiscal deficit.

The way that a country typically reduces a fiscal deficit is by running at surplus (aka exporting more than it is importing). The US is far from running at a surplus and the fiscal deficit is in bad shape with debt levels running at 125% of GDP.

So, the only real solution to solving the debt problem is by inflating the debt away.

Meaning, making money so worthless that the debt becomes worthless as well.

Let that sink in for a minute…

When you think about from this perspective, you start to understand the high degree of inflation that could become the new norm.

The table above shows the inflation rate needed to reach healthy debt to GDP levels assuming spending stays constant and real GDP growth is 0%.

Death to Bonds

If I were to write a guide on how to crash the US Treasury market, it would be a simple four part process.

Sound familiar?

That’s because ALL of these things are currently taking place.

Steps 1 and 2 are slowing economic growth and steps 3 and 4 are creating systemic inflation that the Fed can do very little to stop. All while real incomes are being cut as rising interest rates slash consumer spending.

The result?

Death to bonds.

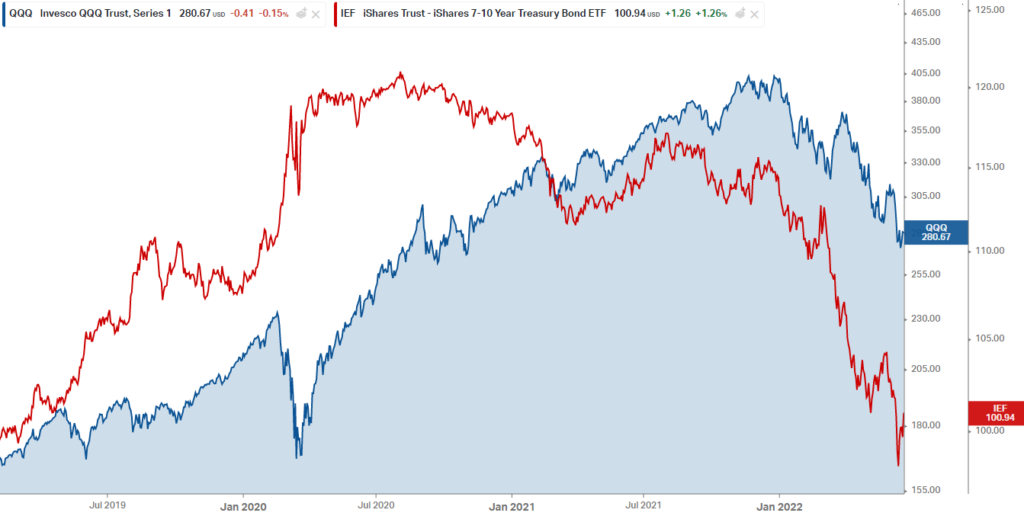

Since the pandemic started, US Treasuries have been highly correlated to equity markets, which you can see in the chart below. The NASDAQ is in blue and US Treasuries in red.

If the bond market is dead, where will people find solace?

I think that answer HAS to be GOLD. (especially considering the recent implosion of bitcoin)

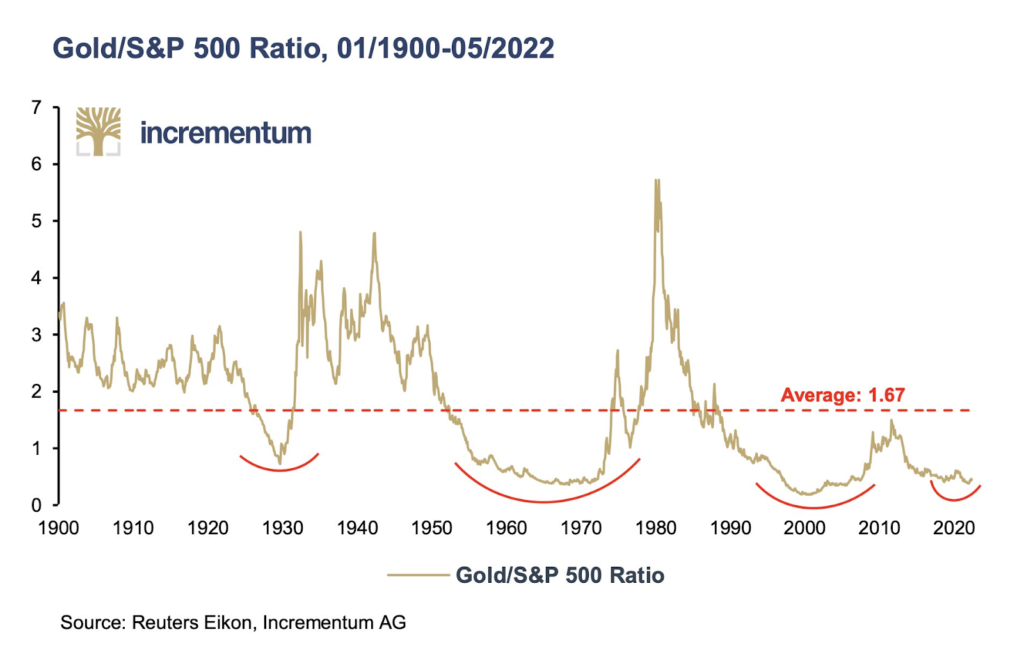

According to Incrementum, gold could more than triple against the S&P 500 if it reaches its 122-year median of 1.67 over the next ten years as the ratio is at 0.47 today.

One last thought to keep in mind.

Gold will likely not take off until the general investor loses faith in bonds, stocks, and the general economy. This is a long process, and we are still likely +8 months away from that becoming a reality, but when the move happens it will be fast and violent.

Prepare accordingly my friends.

CIO; Editor

Head of Research

“Real” assets are assets with an intrinsic physical value due to their substance.

This includes precious metals, commodities, natural resources, transportation infrastructure (roads, airports, railroads), land, and real estate.

Basically everything we do here at Ri.

Many investors include real assets (or should be) in a diversified portfolio due to a relatively low correlation with financial assets, such as stocks and bonds.

But the world has changed… Today it’s questionable if real estate can still be considered a “real asset” asset class.

Since quantitative easing began flooding the market with cheap and easy money from December of 2008, real estate has had a high correlation with the stock market. Cheap money turned houses from a place you keep your kids/stuff in to an “investment” for ordinary people…

Today average home prices have a 60% correlation to the stock market. 60% might not sound like a particularly high correlation rate, but when we put on our data science glasses (and look at the t-scores and p-values), this is a very significant. In simple terms, it means that during months when housing prices are down, there is a very high probability that the stock market will also be down and vice versa.

But more important than the correlation exact % is the fact that it’s been increasing.

Prior to 2008, the correlation between the stock market and housing prices was 28%; in other words – not correlated (housing prices and stock prices were not related – the stock market was not the economy).

Since 2008 housing has been “financialized” – the values of homes are no longer based on supply and demand (wages and housing supply). Housing has turned into a leveraged investment class based on the premise that the future value of a house will rise because someday another buyer will pay more for the house than you.

Inflation is at 8.6% and the average cap rate on real estate is about 5% in most major cities. The cap rate is the yearly return in cash flow (aka rent) that an investor expects to make on a property.

Real estate investors now have a negative real yield on their investments.

Why should you care?

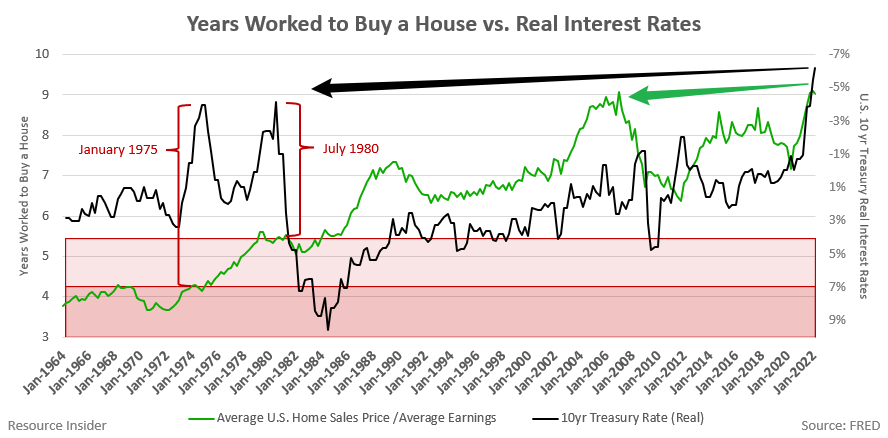

The last time real interest rates (in black) were at comparable levels was in January 1975 and July 1980. At that time, the cost of purchasing a family home, in terms of average annual salary (in green below), was 4.26 years and 5.43 years respectively. That means the average home cost about 5x the average salary.

Today, the average cost of buying a home in the USA is 9.09X the average salary. This is greater than the peak of the 2007 housing bubble.

There are two ways that this could play out:

Either way, it indicates that the housing market is on track for a correction. And given the correlation we discussed earlier, it’s very possible the stock market is headed for a similar fate. It also means that housing is not a “real asset”.

What remains uncorrelated?

Real real assets.

Real assets tend to be uncorrelated because they are driven by supply and demand fundamentals rather than market sentiment (aka they’re based on reality).

This tends to mean more resilient cash flow underpinned by inherent value that protects wealth in times of volatility. It costs a certain amount of $$ to mine a pound of copper or pump a barrel of oil, thus they are unquestionably worth something… unlike, say, an app that acts as the “Uber of Water Fountains” (yes, this is real… sadly).

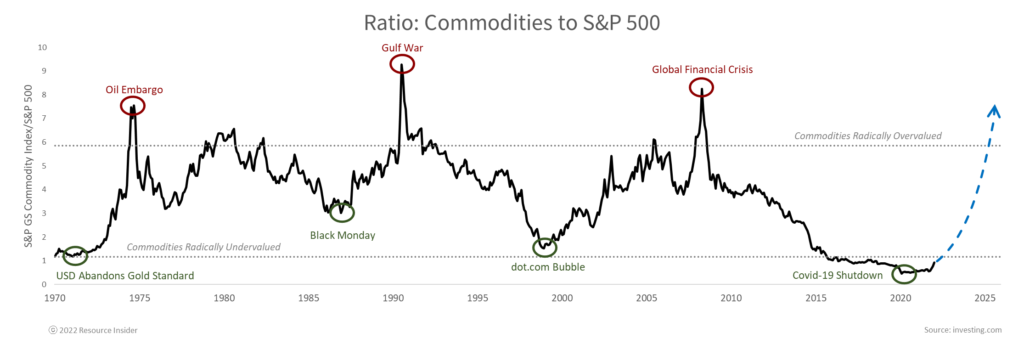

I believe we are on the cusp of seeing the below chart revert to the mean. Commodities and real assets are set to outperform other asset classes and thy’ve got a LOT of catching up to do.

CIO; Editor

Head of Research

I am not saying that a recession is imminent, but one may be lurking around the corner; and if it’s not a recession, it’s probably recession’s cousin stagflation.

Let’s take a quick look at what we’re seeing.

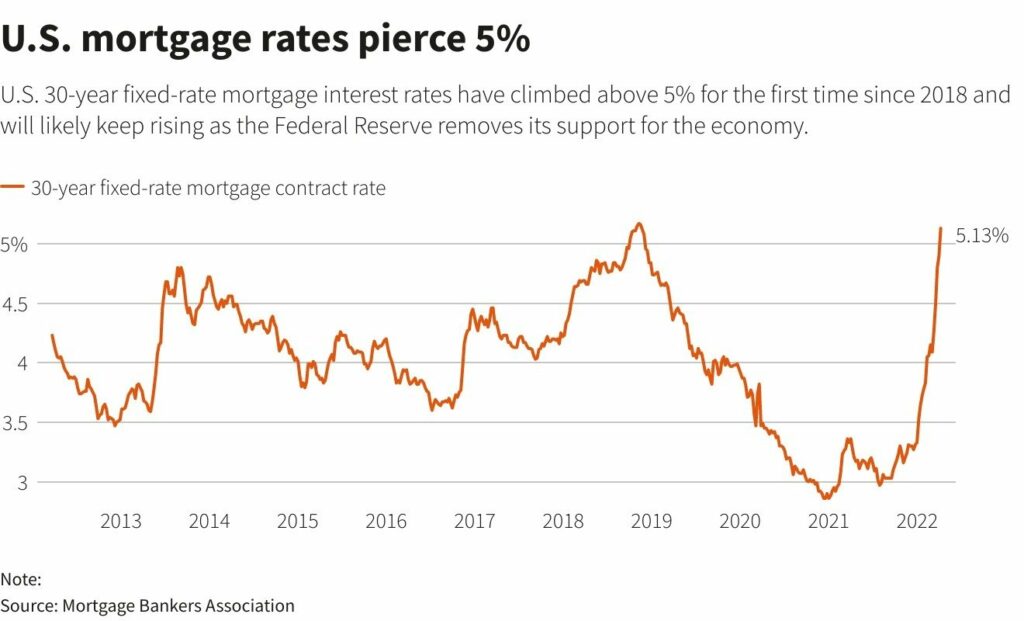

Mortgage Rates – Mortgage rates are now above 5% and are set to continue rising as the Federal Reserve has an aggressive rate schedule of rate hikes planned for 2022. This is important because the Fed is just starting its rate hike cycle.

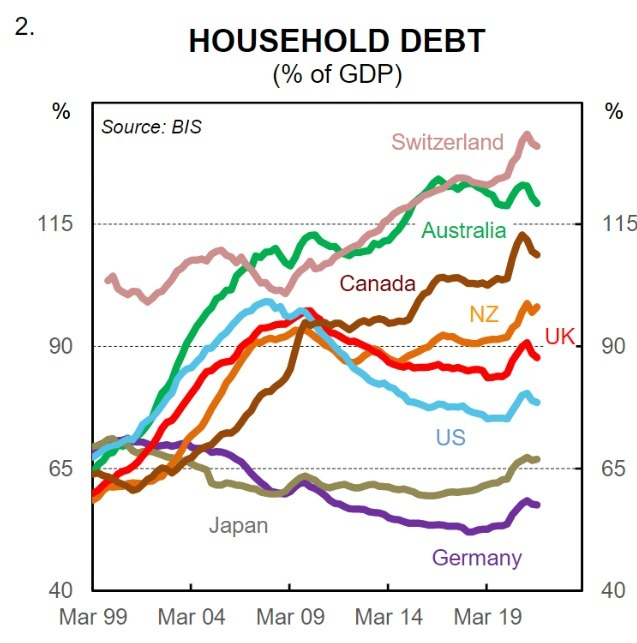

Household Debt – Total household debt is above 100% of GDP in countries such as Canada, Australia, and Switzerland (Meaning: the people owe more than the total country’s GDP). Higher Fed rates also mean higher revolving and floating debt rates for households.

Producer Price Index (PPI) – Price index that measures the changes in prices received by domestic producers. In other words, what producers of goods pay for their raw materials. Year over year % change in PPI is now the highest it has been since the early 80s.

The Chairman of Restoration Hardware said it plainly:

“I don’t think anybody really understands what’s coming from an inflation point of view, because either businesses are going to make a lot less money or they’re going to raise their prices. And I don’t think anybody really understands how high prices are going to go everywhere.”

Some people remain bullish broader equities based on the idea that we are at peak inflation. I don’t see that as a reality as long as PPI keeps surging, because we have 2 options:

What is my takeaway from all of this?

The world is in a very precarious position. The pundits that said “don’t fight the Fed” are now fighting the Fed. The same people who said the consumer is strong with 1.8% inflation are saying they’re still strong at 8.5% inflation.

My point is we’re not only seeing perma-bulls we’re seeing perma-BS, and there are already warnings of a flagging market. Netflix is ~70% off its highs, wiping out 4 years of gains in a few weeks. JP Morgan shares are down ~40% after last week’s earnings showed a slide in profits.

You can see from the chart below that JPM’s stock is highly correlated to the S&P 500. Are these stocks the proverbial canary in a coal mine?

That remains to be seen.

I do not know if the market will sell off tomorrow, in 7 months, or if it’ll mostly trade sideways for the next few years.

What I do know, is that when the market turns over, it will be time to own precious metals. I am a firm believer in gold as an antifragile investment – which we have talked about at length over the past several months.

“Antifragile is a property of systems in which they increase in capability to thrive as a result of stressors, shocks, volatility, noise, mistakes, faults, attacks, or failures.” – Nassim Taleb

For gold, this means that as volatility and uncertainty increase gold strengthens.

The world is entering tumultuous times. I know many of you are disappointed in the recent performance of precious metals miners, but I expect the tides to be turning over sooner than later.

CIO; Editor

Head of Research

Golden Shield – What a Result!!

Golden Shield drilled 50 m grading at 9.1 g/t gold at Mazaoa Hill, Marudi. This is possibly the best drill result that we have seen out of any Ri holding to date (rivaled only by Vizsla).

Those of you that have watched my podcast with Francis MacDonald will remember that he talks about a concept called GT or Grade Thickness. (I highly recommend watching to learn about this metric).

GT = grade (g/t) x thickness of a drill hole (m)

It is important to note that thickness isn’t the entire length of the drill hole, but the portion of the drill hole that mineralization occurs over.

In this scenario, the GT = 455 = 9.1 g/t x 50 m.

To put this into perspective, the majority of:

To capture the majority of +5Moz deposits, discovery intersects should have +10m of mineralized rock. This is because, for big deposits, you generally don’t want to be chasing narrow high-grade veins. It is more profitable to mine larger wide veins.

A GT of 455 is 3.4 times higher than the much sought-after 134 GT metric.

Equally importantly the “new discovery” is not a “twinned hole” or simply re-drilling a previously known deposit, this hole represents a meaningful expansion of the known mineralization. Simply put, this is a banging drill hole and indicates that there is probably a lot more gold at Marudi than previously expected.

Leo Hathaway, the executive chairman, who has found multiple gold mines working with Ross Beaty, said that this is the best drill result he has ever seen out of an initial drill program.

My comment: YESSSSSSSS!!!!!

The share price has bounced back to ~$0.80, more muted than we’d like to see, but remember this company is not yet listed on the OTC markets, meaning it is challenging for USA inventors to buy this stock. I expect significant buying when the OTC cross-listing is complete (soon I’m told!).

In summary: I’m very excited about what’s happening at GSRI.

Congrats to all Members who participated in this deal, I expect our patience will pay off!

What We‘ve Been Waiting for… Unfortunately.

Over the past decade, as tech stocks reached insane heights, the world seemed to forget that we actually need commodities to, you know, do anything.

But such is the fickle nature of the markets.

Commodity markets are cyclical, the pendulum swings from side to side as the market tries to balance at an equilibrium point. For the past several years the pendulum has been artificially pushed in one direction… But now it’s swinging back with a vengeance.

Fortunately at Ri, we’re ready for this violent move.

It was easy to predict as the world has trended away from globalization towards a protectionist/nationalist view.

We saw examples of this with:

The geopolitical battle for economic dominance has evolved into an all-out war. The Ukrainian war is showing signs that it is not just about Ukraine. It’s not even Russian vs. American. More accurately, it is about authoritarian empires vs. the democratic West.

Whether this specific conflict in Ukraine escalates or cools off, the world is forever changed.

The fissures that are growing each day are not easily healed. The damaging impact of sanctions and supply chain disruptions will have far-reaching consequences. Alliances are being formed for the decades to come that will influence trade, travel, economic activity, and global power dynamics.

Globalization has been dealt a mortal blow, as have the disinflationary benefits that accompany it. The financial implications are immeasurable and compounding daily.

The world has entered an environment where energy and food independence is a top priority. A key component of global power will be the control of critical commodities and resources. China has been aware of this for a long time and controls significant mineral, energy, and agricultural resources globally, Russia is positioned as an energy and resource nation – the West, after decades of neglect, has a long way to catch up.

It will take years for this to become a reality. Expect much higher costs (inflation) and a continued shortage of goods we used to take for granted. Each of these “ruptures” will have second and third-order effects the impacts of which are as yet unknown.

But the coming chaos also represents one of the greatest investment opportunities of our generation.

Bear down.

Commodities price movement is accelerating rapidly.

But, commodity equities have barely budged. Believe me – this is a good thing for us.

Miners, especially junior miners, are always delayed when commodities start to run, but when they do move it tends to be violent. Commodity runs very often coincide with global uncertainty, in this scenario capital pulls out of the market and assesses where to “re-deploy” and the answer: The companies that actually produce commodities.

And, there is a long way to go for the relationship between the S&P 500 and commodities to normalize. Even with many commodity prices reaching new all-time highs, the data suggests that the real move in commodities is just getting started.

(Data as of March 7, 2022)

We have an unbelievable buying window, and I intend to take full advantage of it.

CIO; Editor

Head of Research

RESOURCE INSIDER, IVALDI VENTURE CAPITAL LTD.

1090 West Georgia Street, Suite 700, Vancouver, BC, V6E 3V7